Short, working definitions of the terms used in this guide, written

for product and engineering leaders rather than compliance officers.

- KYC (Know Your Customer)

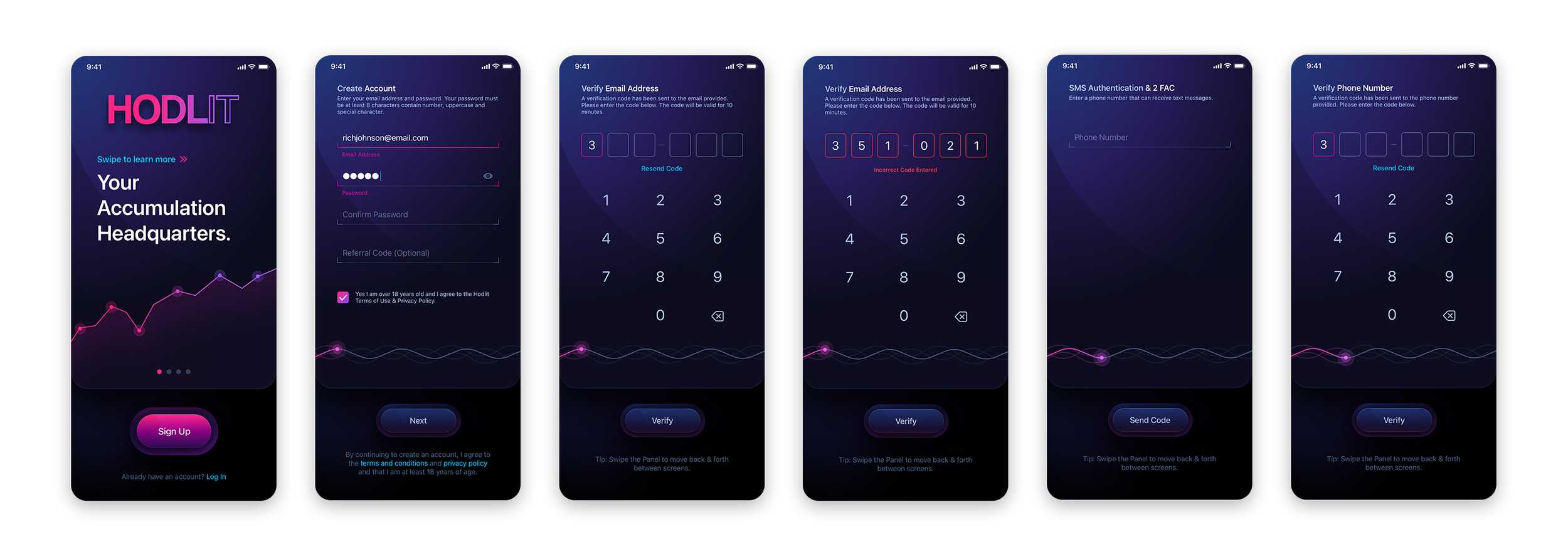

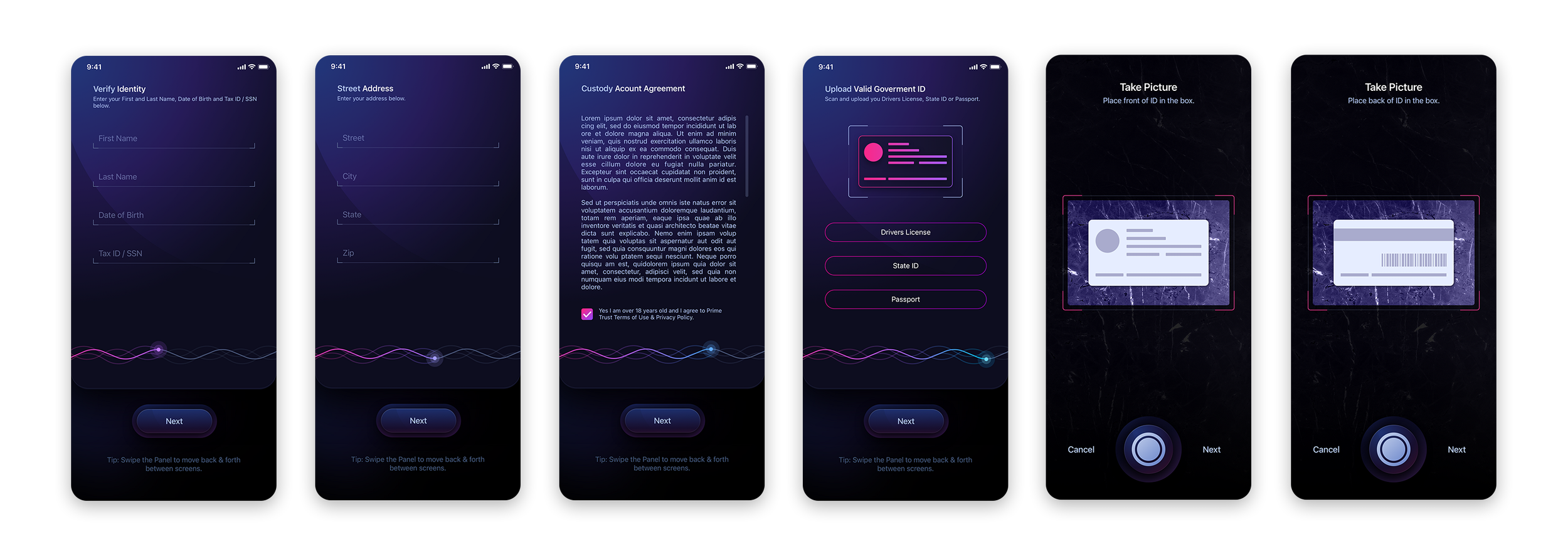

- The regulatory requirement that financial products verify who their users are, typically through identity documents, personal information, and liveness checks. It is one of the largest sources of onboarding friction and drop-off.

- KYB (Know Your Business)

- The business-account equivalent of KYC, verifying a company’s identity, ownership, and legitimacy. It adds document, ownership, and multi-party complexity to business fintech onboarding.

- AML (Anti-Money Laundering)

- The body of rules requiring financial products to monitor, flag, and report suspicious activity. It is frequently the unseen reason behind holds, reviews, and account restrictions that interfaces must explain clearly.

- Liveness Check

- A verification step, usually a selfie or short video, confirming that a real, present person is completing identity verification rather than using a photograph or recording.

- Account Aggregator

- A third-party service that connects a fintech product to a user’s accounts at other institutions, enabling account linking, balance retrieval, and access to transaction data.

- Open Banking

- A framework, formalized to varying degrees across markets, that lets consumers share financial data with third-party products through secure, consent-based connections.

- PCI DSS

- The security standard governing how products handle payment-card data. It shapes interface decisions such as hosted card fields, masking, and what a product may display or store.

- PSD2

- A European payments regulation that, among other requirements, mandates strong customer authentication. It is a major driver of step-up verification patterns in products serving European users.

- MFA (Multi-Factor Authentication)

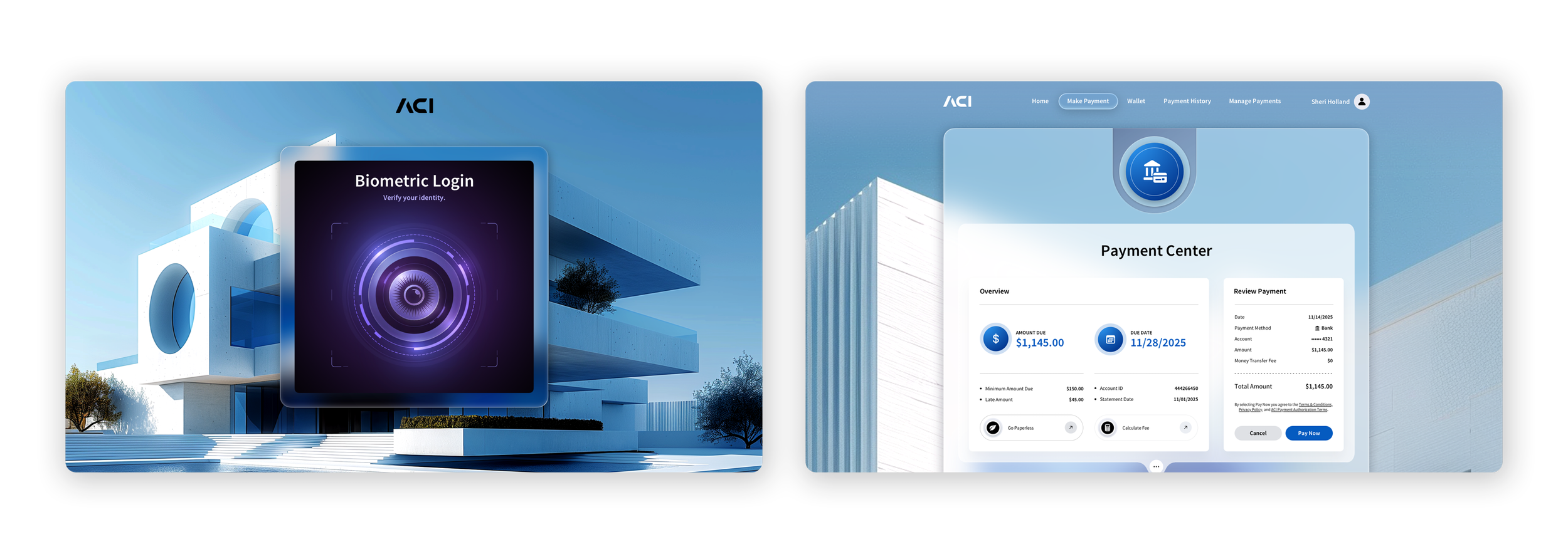

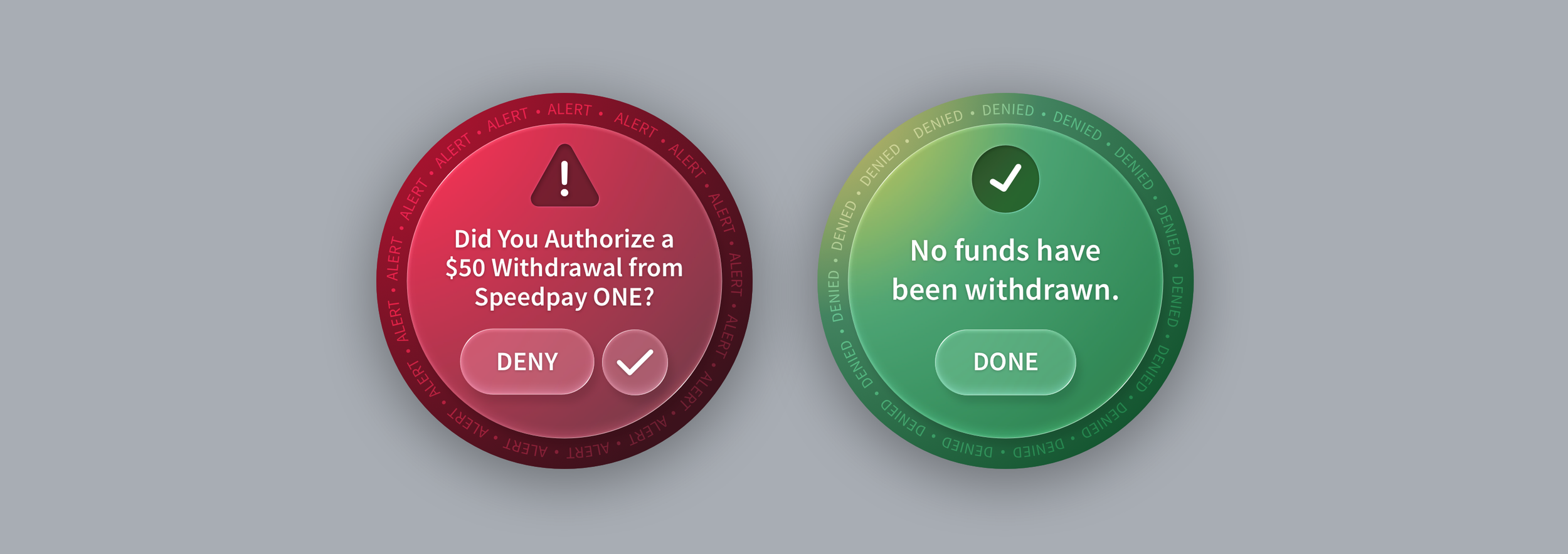

- A security method requiring more than one form of verification, such as something the user knows, owns, or is, to authenticate a user or approve an action.

- Step-Up Authentication

- Applying stronger verification only when the risk of an action warrants it, such as a large transfer, credential change, or sign-in from a new device, rather than applying the same friction everywhere.

- Passkey

- A cryptographic, phishing-resistant replacement for a password that is typically unlocked through device biometrics or a device PIN.

- Tokenization

- Replacing sensitive data, such as a card number, with a non-sensitive token so a product can reference the payment instrument without exposing or storing its real details.

- Gas / Gas Fee

- The fee paid to process a transaction or smart-contract action on Ethereum and other compatible blockchain networks. The amount can change depending on network demand and the complexity of the action.

- ACH

- The United States bank-to-bank transfer network. Its settlement delays are one reason financial interfaces need honest pending and processing states.

- Settlement

- The point at which transferred funds actually and finally move between institutions. Settlement may happen later than the user-facing confirmation, and the interface must communicate that gap honestly.

- Chargeback

- A card-transaction reversal initiated through the user’s bank, triggering a formal dispute process between financial institutions and merchants.

- Dispute

- The user-initiated process of contesting a transaction. It is one of the longest-running and most opaque flows in financial products, and a major trust moment when designed transparently.

- Reason Code

- A standardized code explaining why a transaction was declined, flagged, or reversed. The interface must translate that internal code into language the user can understand and act on.

- Maker-Checker

- An enterprise control pattern requiring one authorized person to initiate a financial action and a different authorized person to approve it before execution.

- Dark Pattern

- An interface pattern that manipulates users into actions serving the business at their expense, such as hidden costs, pressure tactics, deceptive defaults, or false urgency. In financial products, dark patterns directly consume trust.

- Progressive Disclosure

- Showing summary information first and revealing greater depth on demand. It is a core technique for keeping dense financial interfaces understandable without removing information users need.

- Tabular Figures

- Numerals designed to occupy equal width so digits align in columns. They are essential for scannable financial tables and one of the quiet markers of financial-grade typography.

- WCAG

- The Web Content Accessibility Guidelines, widely used as the practical baseline for digital accessibility in financial services, procurement, and compliance review.